Taxable Income Income tax shall be imposed on the income from rental of buildings.

Tax Rate

The tax payable on rented houses shall be charged, levied and collected at the following rates:

(a) on income of bodies thirty percent (30%) of taxable income,

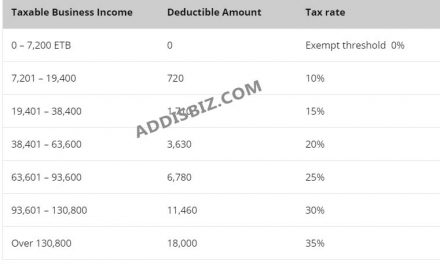

(b) on income of persons according to the Schedule B (here under)

| Taxable Income from rental (Per year-birr) | Income tax payable |

| 0 – 7,200 | 0% |

| 7,201 – 19,800 | 10% |

| 19,801 – 38,400 | 15% |

| 38,401 – 63,000 | 20% |

| 63,001 – 93,600 | 25% |

| 93,601 – 130,800 | 30% |

| Over 130,800 | 35% |

Determination of Income

1) Income from rental of building shall be computed as follows:

(a) if the tax payer leased furnished quarters the amounts received attributable to the lease of furniture and equipment shall be included in income.

(b) sub-lessors shall pay the tax on the difference between income from sub-leasing and.the rent paid to the lessor, provided that the amount received from the sub-lessor is greater than the amount payable to the lessor.

(c) the following amounts shall be deducted from income in computing taxable income:

(i) taxes paid with respect !o the land and buildings being leased; except income taxes; and

(ii) for taxpayers not maintaining books of account, one fifth (1/5) of “the gross income received as rent for buildings furniture and equipment as an allowance for repairs, maintenance and depreciation of such buildings, furniture and equipment;

(iii) for taxpayers maintaining books of account, the expenses incurred in earning, securing, and maintaining rental income, to the extent that the expenses can be proven by the taxpayer and subject to the limitations specified by this Proclamation; deductible expenses include (but are not limited to) the cost of lease (rent) of land, repairs, maintenance, and depreciation of buildings, furniture and equipment in accordance with Article 23 of this Proclamation as well as interest on bank loans, insurance premiums.

2) The owner of a building who allows a lessee to sub-lease is liable for the payment of the tax for which the sub-lessor is liable, in the event the sub-lessor fails to pay.

3) At the earlier of the time construction of a rental building is completed or when the building is rented, the owner and the builder are required to notify the administration of the kebele in which the building is situated about such completion and the name, address, and tax identification number of the person (or persons) subject to tax on income from rental of the building. The kebele administration has the obligation to communicate this information or information obtained by the administrations own initiative to the appropriate tax authority.

{kind=link}